What I am seeing is the net capital gain on my W-2, and the net capital gain on the 1099-B, and I am being asked to pay the tax on 2X despite only getting X as actual money.

What’s the “net capital gain” here? Like, the different kinds of stock sales here should have somewhat different treatment:

- RSUs: this is stock that is first given to you (ordinary income, not a capital gain) that you later sell, potentially with a profit relative to the stock price when it was given to you (this is a capital gain)

- ESPP: forget how these are treated tax-wise as it’s been a long time since I worked at a company with one of these, but similarly I imagine there’s an ordinary-income component here for the money you use to initially purchase the stocks and then a capital gain on the profit

- stock options: I think these are usually untaxed if ISOs and you don’t exercise them? (but it’s been a minute since I got options at a job)

I’d expect to see the ordinary income parts on your W-2 (after all, it’s not like your employer knows at what price you later sold the stock), and for the 1099-B to log acquisition & sales of stock and capture the difference (capital gain/loss).

I don’t know anything about taxes but are there other people at work who have done whatever it was you did with your securities before? Seems like you wouldn’t be first to plug however the company reported it into TurboTax

RSUs should have a cost basis of $0. It’s just stock given to me. ESPP, I set aside X% of my salary, and then twice a year I get to buy stock with it at a Y% discount of the market rate that day. I pay ordinary income taxes on the income set aside, and (usually short term, aka ordinary income) capital gains for what it sells over what I paid for it. Options are worthless when you get them, I earn the difference in current price over the option price when I sell them, and they’re worthless if the current price is lower than the option price.

One key detail I forgot to mention is that when looking at the transaction history from the brokerage that handles this, I paid withholding on the option sales. And my employer definitely knows when and what price I sold the stock for. All transactions in company stock in or out have to be through one company-branded account on this one brokerage, and I have to get preclearance authorization to sell anything.

I suppose, but basically no one talks about this. I kinda hate to be the first.

OK, this was really helpful though. I should have realized that the RSU line item on the W2 was the cost basis, not the net. I actually sold those RSUs for a loss overall, so that may help the bottom line.

Wookie gets a big tax bill-but looks to turn it into a refund.

2 Likes

I mean, I realize it’s a blessing and a privilege to have an unexpectedly large tax bill. There’s no denying I got a windfall, and it’s better than a lot of common alternatives. I don’t feel compelled to pay double than what I owe and that what other people like me might pay. It also sucks to pay a higher percentage than fucking billionaires.

2 Likes

I don’t think this is correct; if you hold your RSUs for X amount of time (whatever the long-term capital gains threshold is) it doesn’t suddenly all become LTCG. Receiving the RSUs is an immediately taxable event at ordinary income rates based on their market value at that time. If you hold them for a nonzero period of time and then sell, that incurs a separate capital loss or gain depending on whether they went up or down since you got them.

You should be paying taxes at ordinary income rates on the value of the stock when you received it and at capital gains rates for any gains over that initial value. I think.

What makes it complex, I believe, is they auto-sell shares to cover the taxes when they’re awarded?

Sometimes, yes. It looks like at least for the options. Not the RSUs, I don’t think, which are labeled “taxes due” while the options are labeled “taxes paid.”

Now that this is officially Wookie’s Tax Fuckup Live Blog, I’m making progress. I’ve got the RSUs and NQOs squared away. It’s the ESPP that is confusing. Googling around, since I sold my ESPP shares mere days after issue, this should be a non-qualified short term capital gain. My company offers look back and a 15% discount on shares (this is the main cause of the windfall) with purchases twice a year, so it seems like my company should report (share price at issue - price I actually paid) * # ESPP shares on my W-2, since that’s the additional compensation at the time the ESPP shares are issued, and then I just put on my tax form, “Yo, IRS agent, I promise that the cost basis for this transaction is not what that 1099-B says. It’s actually this other number, so that big ol’ windfall is actually a capital loss,” as the stock did go down somewhat from the day it was issued to the day a few days later that I sold. And they are supposed to believe me.

But I don’t think I believe me, because the number reported as ESPP income on my W-2 is not equal to what I calculate the summed (share price at issue - price I actually paid) * # ESPP shares for the two transactions. It’s roughly half that, but not equal to either one single transaction, either. Maybe there’s a cap on ESPP compensation that gets reported this way? Maybe just split the reported income between the two and call it a day?

1 Like

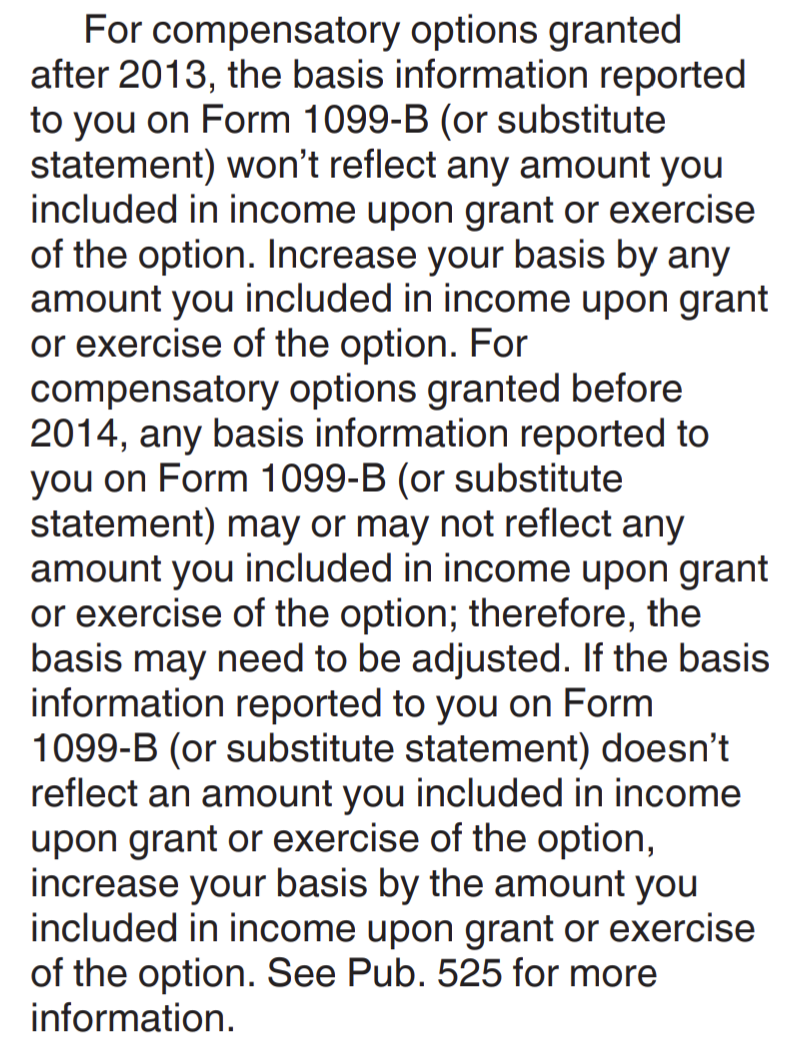

IANAA but I believe this is a common thing, so much so that there’s an entire column for it on form 8949. A 1099-B can show an incorrect basis for all kinds of valid reasons. The process for fixing it is to report the transaction on form 8949 with the basis as reported to the IRS, then make an adjustment to get what you think your basis should be, then report that corrected amount on your schedule D. In some cases the reason for the discrepancy is so common that the IRS has written specific rules for finding the adjustment, which you can find in the instructions for form 8949, or a publication referenced in those instructions, and I assume turbo tax will have these programmed in if you can find the question tree to get you there. Does this look like the correct description of your situation? It’s one of the cases listed in the 8949 instructions.

Yeah, to be a bit more clear, I’m at least trying to do this correct in good faith, and I’m pretty sure I"m supposed to put in a new basis number because that income got recorded elsewhere lest I get rekt by paying taxes on the same windfall twice, but this thing where you can just change the basis to some new number seems like an invitation for scoundrels. The number I put there doesn’t seem like it has to be backed up by anything on my W-2 or 1099-B or my 3922 (which is itself inconsistent with my W-2 according to how I thought this all was supposed to be reported).

OK, here’s something super frustrating. “Aha!” I think. “I did the same thing in 2022 as I did in 2021 - sell my RSUs, NQOs, and ESPP shares right away. I should be able to compare 2022 to 2021 to perhaps gain some insight into how that ESPP income number on my W-2 was calculated!”

There’s no ESPP entry on my W-2 in 2022. Wat.

Alright, I think the resolution here is to just bump up the wages entry from my W-2 quasi-artificially to reflect the ESPP wages that should have been there, increase the ESPP annotation (that doesn’t mean anything, but just for annotation), then report the ESPP sale as a loss, update the information for NQO and RSU, and then pay the ensuing bill. It’s, uh, not great, but it’s only about 1/3 of what the IRS would have me pay if I hadn’t gone through all this trouble.

Now I get to work all this out again for 2022. Weeeeeeeeeeeeee

1 Like

What does this mean? If your w2 is incorrect you can ask HR to correct it. If they don’t and you’re still confident it’s an error there’s a specific way to account for it on your tax return. Quasi-artificial seems like a bad idea. Any numbers reported on w2’s and 1099’s absolutely must show up exactly on your tax return somewhere or you’re 100% getting audited.

Personally feel like you 100% should get an accountant

2 Likes

+1 on this. I think you’ve definitely crossed into ‘paying a CPA to do your taxes is +EV’ territory here… and I’m a guy who has always done his own semi complex taxes.

1 Like

From what I’d seen, increasing your wages compared with your W2 isn’t an issue, but I suppose I could change the basis calcuation of the ESPP shares instead? I dunno man, I’m pretty sure I got what I owe right, but documenting it all correctly is complicated.