Speaking of…

Thanks, Biden!

We are at the beginning of the beginning of the end, and I have no confidence in our leaders to make the right decisions.

In 2008 we didn’t stimulate quite enough and in 2020-2021 we overcorrected and stimulated too much (I admit to wrongly supporting the overstimulation).

In 2023, we are in the process of making two simultaneous overcorrections 1) overtightening as a reaction to stimulating too much in 2020-21 and assuming Cuse is correct, inflation from the Ukraine war that the Fed should ignore 2) an unreasonable aversion to “bailouts” as a result of the 2008 financial crisis and the political fallout.

If we don’t correct course asap then things will end up somewhere between bad and very, very, very bad.

By the way, if you aren’t aware, the CEO of SVB was on the board of directors at the San Francisco Fed. The idea that SVB was caught off guard by all of this is just not rooted in fact.

Still avoiding giving falsifiable numerical predictions about what will actually happen, so your musings are completely useless.

Give us sp500 numbers or you will claim to be right no matter what happens

Again, I couldn’t give two shits what happens to the CEO of SVB, he obviously shouldn’t get a penny throw him in jail for all I care. What I care about is the attitude that the Fed is on the right path and making the right moves when they absolutely are not. Does pointing out that Trump picked Powell help?

My opinion is that Powell waited too long to hike rates and shouldn’t stop yet. My opinion is that 0% interest is a perverse market manipulation that should only be used in extreme situations and should never persist long term. So this has nothing do with Powell himself or who picked him.

Do you have money at SVB or does your employer or something? You seem really charged up about this and I’m not sure why anyone should be this upset over SVB clients losing 10-15% of their cash when the dust settles.

By the way, let me lay out a moral hazard of backstopping all the SVB clients.

Apparently most/all of the companies Peter Thiel backed were banking with SVB. That means he controlled a huge percentage of their deposits, and could likely single handedly cause a run that would knock SVB out of business. I don’t even want to know the amount of money he could make by taking a leveraged short position on SVB while causing that run. But it’s got to be massive, and that’s before considering that he could also take a long position on short-term treasuries to profit off the flight to safety.

Now, consider that he was likely invested in a bunch of startups that were losing money, that could only survive to profitability in a low/zero interest environment, and that were thus headed for failure in the next year or two given the interest rate environment.

Is it crazy to think he might have caused this for his own profit? If so, he should go to jail, and the least that should happen is that the businesses banking with SVB shouldn’t be made whole on whatever % of their deposits is lost.

Is that a bit unfair to the businesses not involved in this? Sure. But, free markets, etc, etc. How many of those businesses supported stricter regulations and lower yields due to higher insurance costs for banks?

At least two midsize banks failing after the 16th biggest bank failed in a matter of 6 days is a falsifiable prediction and a clear sign that things are going off the rails. Can’t help you if you are too stubborn/dense to admit or see that.

As far what the S&P will do, would bet it will be at least down 5% this week if we wake up with SVB in normal FDIC liquidation tomorrow. Sure you will say that is no big deal either, falsifiable prediction of 15% in one week or stfu!

Looks like you may get your wish:

Pretty annoying IMO. And I also don’t think the S&P being down 5% this week would be a sign of anything being off the rails. That’s not that unusual lately. The entire market was in a bubble, still may be.

Saying spy will be X if Y happens is useless. You need to predict what will actually happen if you think you have a point. Unless your point is that you think the fed/regulators are going to handle the situation appropriately to mitigate systemic risk.

I went into the weekend assuming the Fed would absolutely backstop SVB because it so obviously the correct move and then saw reports that they might not and idiots cheering them on. That is where we are.

I mean his point seems to be that he thinks there will be a run on many US banks tomorrow, which will collapse the US banking system, which will collapse our economy and the stock market. It’s not, like, impossible.

I’d argue that it would be easy to prevent if the FDIC just came out and said, “Look, we’re going to backstop 100% of the deposits at any bank that has a positive balance sheet and was not engaged in risky behavior. We’ve stress tested the following banks and they’re fine,” followed by a list of all banks subjected to mandatory stress testing. They could then offer to stress test any smaller bank that wanted to.

But still haven’t heard your prediction of what you believe will actually happen?

Your posts read like this is an immediate massively huge disaster over next 1-2 days to US economy but also that you think the regulators/fed will ultimately prevent a major disaster. So are we getting the massive disaster this week or not?

In my mind if feds/regulators are able to manage this situation that is evidence they have been doing a good job not a bad job. If spy is down like 15%+ at end of week then yeah pretty obvious they really fucked up.

Plenty of experts in the field are saying similar things to what I’m saying. There’s clearly disagreement among intelligent people on this. You don’t need to be an asshole.

My guess is most of the people shrieking for bailouts have a personal stake in SVB depositors getting bailed out. I don’t think most of the people saying no bailout is necessary are personally short those companies, so I’m inclined to side with the “no bailout needed” camp. Plus their arguments make a lot of sense to me. But I am biased on that I love mocking anti-regulatory conservatives/libertarians when they come begging for a handout/bailout for themselves after shitting on poor people constantly.

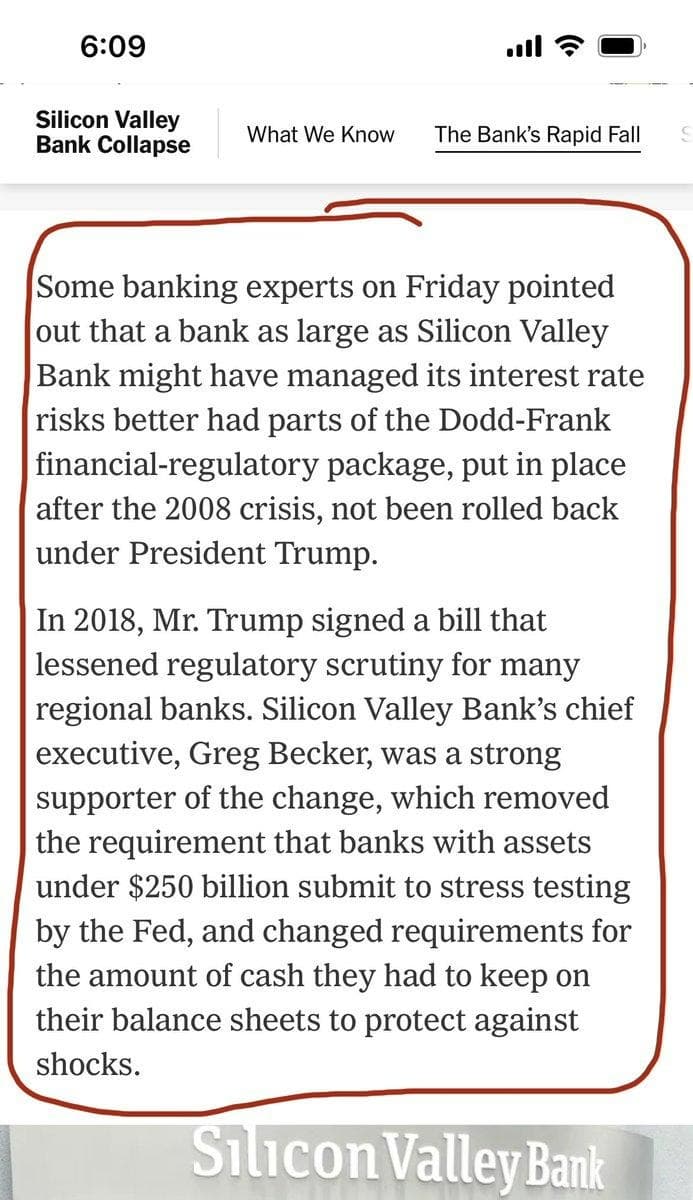

Is it a sign the federal regulators fucked up, or a sign that lawmakers who weakened regulations fucked up? Cause under Trump, banking regulations were rolled back.

This sounds fine to me. (This guy is apparently a huge asshole, though. Not endorsing him just this idea.)

I agree with you that Powell hiked rates too high, and should ease off on threats to raise them higher. I just don’t think we should bail out SVB or their creditors.

But I don’t think Powell has been incompetent, the inflation had more to do with COVID era supplier and consumer behavior and the fiscal stimulus than Fed Policy though ZIRP certainly didn’t help.

Me and my company have no money with SVB and trivial indirect exposure to SVB. But that trivial indirect exposure is enough for me to see that everything is connected and laughing at the depositors at SVB and the next midsize banks to fall is rooting for the leopard to eat your face.

The depositors at SVB aren’t facing failure. They’re facing a 10-15% haircut on their cash balances at SVB. As for the next midsize banks to possibly fail, my opinion comes down to what their practices were. If they did nothing wrong and the run was just panic, then I’d say sure backstop all that.