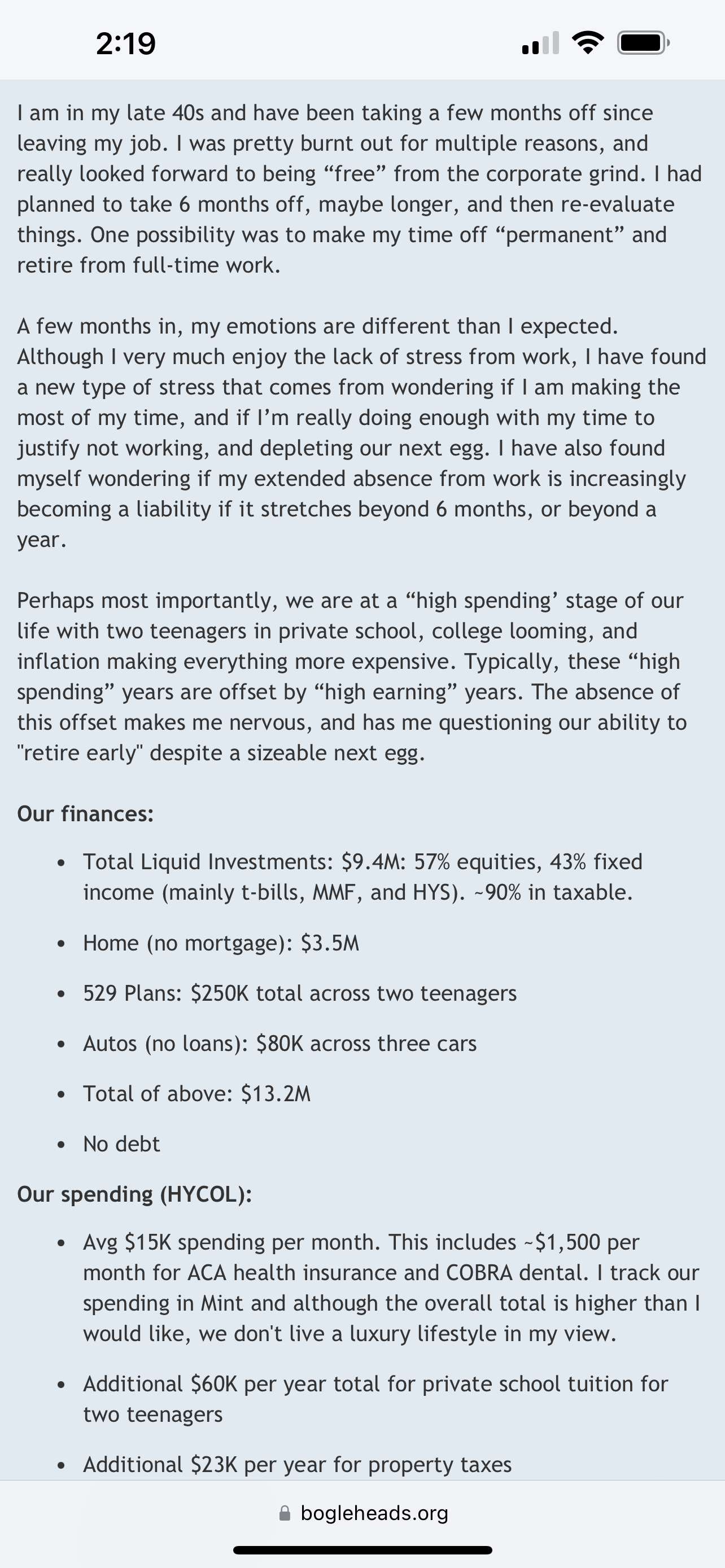

I’m late following up on this: the money ran out after 2 weeks, lol California

How is this part supposed to work?

Here’s a simple example: A moderate-income borrower receives a 20% Dream for All loan on a home that costs $100,000. The loan from the state would be $20,000, and their primary loan would be $80,000. When that borrower pays off the full $80,000 of their primary loan, their home has appreciated in value and is worth $200,000. At that time, the borrower would be required to pay back $20,000 to the state, plus 20% of the appreciated value. Since the home is now worth $100,000 more than what they paid for it, they would be required to pay an additional $20,000 on top of the $20,000 loan amount—for a total of $40,000.

This isn’t when they cash out, but rather when the loan is paid off? That could be a large bill for money they’ve only made on paper.

Ironically he’s at exactly the spot where I plan to transition from working for a living to being a gentleman gambler who does more or less whatever he wants. Based on how things have gone so far I’ll probably make even more money because lol of course that’s how the economy works.

I won’t have to go on bogleheads to get my head patted though. Inherited wealth really is a motherfucker… normal people have to make a ton of very intentional choices to get to that point, and usually if you aren’t an idiot that comes with a ‘ok at X point I’ll have won capitalism and it’s time to execute my exit strategy’. Either you have your number or you don’t. This reads like this is the first time he’s thought about this. That only happens when your whole life you’ve basically just had a go with the flow attitude.

Fucking nobody ever wakes up with 13M dollars by going with the flow and being born even middle class. You go with the flow as a middle class or lower person you wake up at 44 with 25k more in credit card debt than retirement savings, and 10k in negative equity on your car.

100% of these “I’m a millionaire but don’t feel like it” stories involves kids in private school for more than the median national salary.

4 Likes

I don’t understand how someone spending 3 times my take home a month so 6 to um (whatever, I’m not numbers guy) if he was being paid and doesn’t think that’s extravagant AND doesn’t have a house or car payment. I used to be alright with the old “how ever much you make you don’t think you’re rich” but how are dumb fuckers making this much money? How stupid are you to think you can spend almost twice the average salary a year and not be rich?

Which they nearly always also attended ldo.

1 Like

Yeah that’s the thing. If you grew up even a little bit normal you would know. They have no idea because they haven’t ever lived any other way.

The reality distortion field up top is crazy. The reason talking about money is taboo is because rich people don’t want to talk about money. They don’t like the way it makes them look or feel so they simply make it not allowed to talk about personal finances or personal problems.

Fastest way to not be staff for rich people anymore is to make them feel guilty about how little they pay you.

1 Like

If he could do the math, he’d see 10% on that 9.4 million would let him live his current lifestyle and still increase his net-worth by over half a million each year.

1 Like

Even if you go with 4% he’s obviously hit escape velocity. given the private school/college is a temporary expense. He’s only spending like 300-400k a year. Under even the most pessimistic outlooks he’s got fuck you money.

Hilariously the only reason I want to get to a somewhat lower but still stupid rich level is that I want to never have to do anything for money ever again, and I want to be able to stop worrying about it for good. That’s all I want, freedom from the anxiety society has been beating into me since I was a kid getting the shitty free lunch at school.

2 Likes

1 Like

What’s the latest prognosis for ibonds?

what, and end up poor?

Sell them and don’t buy more

1 Like

I don’t think it’s that simple. I plan to max out one more time before 4/27. You can currently lock in a 12-month return of about 5.35%, of course you’ll have to hold them 15 months to keep all that so the annualized rate is lower - about 4.28%. That’s less than you can get in CDs (approx 5.0% to 5.15%), but it beats what’s available in savings accounts.

Then, if inflation goes back up - which is definitely in the realm of possibility - you could hold past the 15 months and see returns that beat a CD.

I don’t currently have my entire emergency fund in I Bonds, so this lets me do so. I like having it hedged against inflation. The new batch will also be at 0.4% fixed rate versus the 0.0% fixed rate my prior I Bonds have, so once they are out of their higher adjusted rate window (still a little ways off based on when I bought them), I can sell those I bonds, hold onto these at 0.4% fixed and see what the adjusted rate does from there.

tldr; if you want to have a 6 month emergency fund (or whatever duration) in something very safe and hedged against inflation, they’re still a viable option.

Am I missing something @riverman? For me, I keep 12 months living expenses in my emergency fund since my income is volatile, and I have to invest my bankroll very safely. Hedging both against inflation seems wise, and the returns here seem close enough for the next 15 months to the best available (essentially) risk-free returns to make it worthwhile.

I do grit my teeth just a tad about buying bonds right before a possible government default, but the real risk there seems to be on the T-bills with maturities in late June through July.

Is there any downside to putting money in VMFXX instead of high-yield savings accounts? Just realized doing so would get me another 0.5% in interest.

Seems like it might be a little less liquid, and that the extra 0.5% is going to be offset slightly by an expense ratio?

But speaking of which, any recommendations for a high yield savings account?

I’ve got Amex which works very well, but I think it lags a little behind on interest rate. Currently 4.0 I think.

Apple is offering 4.15% but for the life of me I can’t figure out how to get money out of it as money and not a gift card…