I participate. I’m not an expert on the counterparty risk but my understanding is also that it’s negligible. As for inviting more selling pressure, IMO very rarely (if ever) should that be a concern, or not enough to outweigh the benefit of collecting free money. The selling pressure mostly cancels with the future buying pressure you’re creating: more shorts means more price support from profit-taking shorts and more rocket fuel from paper-handed shorts. Best of all, having lots of shorts would get your ticker noticed by the sQuEzE crowd on social media, as well as drive up the borrow fee.

Plus like you alluded to, long-term it makes no difference because if the company is successful, the stonk will go up. Contrary to popular reddit opinion, you can’t short Amazon into bankruptcy. If shorts were nearly as powerful as people thought, shorting would be the easiest game ever.

‘I walked away from my $170K job’: This accountant quit at 41 to live off dividends from his $1.25 million portfolio

These “living off the dividends” stories are a pet peeve, people pretend like stock dividends are generated out of thin air.

But this one just compounds the bullshit:

What enabled him to step away and leave so much money on the table? A wife with a great job — and a steady stream of dividends…

LMAO, it’s like the kid who says it’s easy to save $100K for a house downpayment by clipping coupons and also getting a $100K gift from mom and dad.

The story also highlights a dividend-focused ETF as an example:

a worker with a typical salary can still use dividend stocks to accumulate wealth. The ProShares S&P 500 Dividend Aristocrats ETF has delivered an annualized rate of 10.50% over the past 10 years.

This is true, NOBL has a 10yr annualized total return of 10.5%. “This fund focuses on stocks within the S&P 500 that have hiked dividends for at least 25 consecutive years.” That’s cool and everything, but fails to mention that it underperforms the SP500 by a pretty wide margin (SPY 12.6% annualized). Add in the 0.35% expense ratio for NOBL and it seems like pretty bad advice for “wealth accumulation”!

Here’s an idea: open a fund that guarantees to pay a 20% dividend every year and charge a reasonable .5% ER. Put the details in a prospectus that nobody will ever read. Dividend enthusiasts will line up to give you all their money. Then just invest in index funds. It’s win-win since you get rich while they get to tell their golf buddies how they’re “making” 20%. Then shut down the fund after 5 or 6 years because there’s no fucking money left.

Yeah it’s an absolute joke. There are literally enhanced yield mutual funds that buy stuff right before the dividend record date and then sell it. Boomers eat this shit and hold garbage like AT&T for decades because MUH YIELD WENT UP!

I think it’s a bad investment but that’s not even my main gripe. The real issue is people hold this crap for the dividend with no opinion on the company’s future or care for stock price fluctuations.

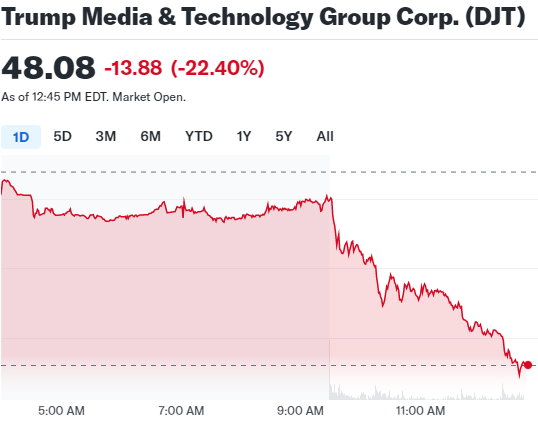

I think the real test will be the first time Trump tries to cash in on any of the stocks. I suppose he could get a loan against them, but what bank is going to accept stock that bad as collateral? I know, I know, “all of them…”

I suppose I’m biased. I’ve been fucking around with SPACs since COVID. Made a ton, gave most of it back and now just follow it because I find this stuff interesting. I would say I treat it like how most people treat sportsbetting.

I think we have enough data at this point to state that any company going public via SPAC instead of IPO is a huge red flag that that company is a scam.

You can still make money off the SPACs by swing trading them, but these are not wise investments.

Much of the net loss appears to come from $39.4 million in interest expense, according to the filing.

DEBT KING! lollll

The company ended 2023 with just $2.7 million in cash on hand, the filing said.

By my back of the napkin math, at their 2023 burn rate, that’s enough to fund like 17 days of operations.

TMTG also disclosed to regulators that the company had identified “material weaknesses in its internal control over financial reporting” when it prepared a previous financial statement for the first three quarters of 2023.

As of Monday, Trump Media said these “identified material weaknesses continue to exist.”

Let’s go right to the official filing, shall we?

The combined financial statements which accompany this Report have been prepared assuming that TMTG will continue as a going concern. As discussed in the report of TMTG’s independent registered public accounting firm and the combined financial statements, TMTG has suffered negative cash flows and recurring losses from operations that raise substantial doubt about its ability to continue as a going concern.

To date, TMTG has financed its operations principally through loans or offerings of securities exempt from the registration requirements of the Securities Act. TMTG’s management believes that capital raised from the Business Combination will be sufficient to retire existing debt and to fund existing operations should projected cash flow be insufficient to fund operations. TMTG may require substantial additional financing at various intervals in order to continue to develop and promote Truth Social, including significant requirements for operating expenses including intellectual property protection and enforcement, for pursuit of regulatory approvals, and for commercialization of Truth Social. TMTG can provide no assurance that additional funding will be available on a timely basis, on terms acceptable to TMTG, or at all. In the event that TMTG is unable to obtain such financing, it will not be able to fully develop and commercialize Truth Social. If TMTG becomes unable to obtain additional capital and to continue as a going concern, it may have to liquidate its assets and the value TMTG receives for its assets in liquidation or dissolution could be significantly lower than the values reflected in TMTG’s financial statements.

I’m imagining what tricks they might have up their sleeve. Like, sell a 90% interest in some Trump building worth $50M for 10 cents on the dollar ($4.5M), then sell a 1% stake in the same building to someone bribing Trump for like $10 on the dollar. Take a 100x “mark to market” increase on the balance sheet to $450M, book $445.5M in “income” and flip a quarterly filing way positive, MAGA morons buy it to the MOOOOOON! Then rug pull.