The lesson might be that there are some industries that are bad to bank. Imagine that it was 2021, and someone was like “do you want to start the Bank of Crypto? What about the Bank of Venture-Backed Tech Startups?” You’d be tempted, right? Those industries had so much money! They seemed cool. If you were their bank — if you were the specialized bank that exclusively focused on those industries — influencers on Twitter would tweet nice things about you, and you’d get invited to fancy parties. Also, as their bank, you’d probably find a way to get a cut of growing industries with lots of potential. Provide banking services to tech startups, get warrants in those startups, get rich when they go public. Provide banking services to crypto exchanges, start some sort of blockchain-based payment network, get rich through the magic of saying “blockchain” a lot.

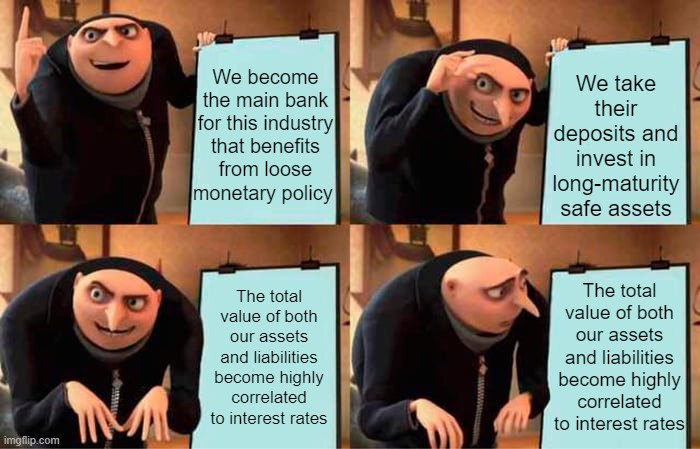

But the structure of being the Bank of Crypto or Startups was a bit rickety. Traditionally, the way a bank works is that it takes deposits from people who have money, and makes loans to people who need money. The weird problem with focusing exclusively on crypto or startups in 2021 is that they had too much money. If you were the Bank of Startups, the main service that you provided to startups is that equity investors would give them a truck full of cash and they’d deposit it at your bank.

…

But the customers didn’t need loans, in part because equity investors kept giving them trucks full of cash and in part because young tech startups tend not to have the fixed assets or recurring cash flows that make for good corporate borrowers. … Customer money keeps coming in, as deposits, but it doesn’t go out, as loans.

So you have all this customer cash, and you need to do something with it. Keeping it in, like, Fed reserves, or Treasury bills, in 2021, was not a great choice; that stuff paid basically no interest, and you want to make money. So you’d buy longer-dated, but also very safe, securities, things like Treasury bonds and agency mortgage-backed securities. We talked yesterday about how this worked out at Silvergate Capital Corp., the actual Bank of Crypto. And as of the end of 2022, Silicon Valley Bank, the actual Bank of Startups, had about $74 billion of loans and about $120 billion of investment securities.

…

The result of this is that, as the Bank of Startups, you were unusually exposed to interest-rate risk. Most banks, when interest rates go up, have to pay more interest on deposits, but get paid more interest on their loans, and end up profiting from rising interest rates. But you, as the Bank of Startups, own a lot of long-duration bonds, and their market value goes down as rates go up. Every bank has some mix of this — every bank borrows short to lend long; that’s what banking is — but many banks end up a bit more balanced than the Bank of Startups.

…

But there is another, subtler, more dangerous exposure to interest rates: You are the Bank of Startups, and startups are a low-interest-rate phenomenon. When interest rates are low everywhere, a dollar in 20 years is about as good as a dollar today, so a startup whose business model is “we will lose money for a decade building artificial intelligence, and then rake in lots of money in the far future” sounds pretty good. When interest rates are higher, a dollar today is better than a dollar tomorrow, so investors want cash flows. When interest rates were low for a long time, and suddenly become high, all the money that was rushing to your customers is suddenly cut off. Your clients who were “obtaining liquidity through liquidity events, such as IPOs, secondary offerings, SPAC fundraising, venture capital investments, acquisitions and other fundraising activities” stop doing that. Your customers keep taking money out of the bank to pay rent and salaries, but they stop depositing new money.

This is all even more true of crypto — I mean, the Fed raised rates once and the entire crypto industry vanished? — but it is not not true of startups. But if some charismatic tech founder had come to you in 2021 and said “I am going to revolutionize the world via [artificial intelligence][robot taxis][flying taxis][space taxis][blockchain],” it might have felt unnatural to reply “nah but what if the Fed raises rates by 0.25%?” This was an industry with a radical vision for the future of humanity, not a bet on interest rates. Turns out it was a bet on interest rates though.